A version of this article originally appeared on RBC Wealth Management Insights.

The Chinese Communist Party (CCP) recently celebrated its 100-year anniversary, highlighting its remarkable longevity even within the context of the country’s 5,000-year history. Few regimes in modern times have remained in power more than 70 years.

Under the Party’s watch, China has experienced a profound metamorphosis—from a poor agrarian country led by Mao Zedong in the 1960s to a global economic titan today. It has given rise to technology giants, built ultramodern infrastructure, brought free-market forces into its economy, and become an integral part of the global supply chain. Throughout this process, the CCP has successfully changed tack to adapt to circumstances and foster rapid modernization.

Now, despite its might, China is challenged by two trends that have become entrenched over the past decade: a persistent decline in the working-age population, and a decreasing rate of productivity growth. A confluence of these forces could halve China’s economic growth compared to recent levels, according to World Bank forecasts that see growth declining to 4.5 per cent per annum in 2019–2031 and falling further to 3.5 per cent the following decade.

A productivity challenge

China’s demographic challenge, largely a product of the “one child” policy it pursued from 1979 to 2015, is well documented. The rapid aging of the country’s citizens, more than a third of whom are now over age 50, recently led the government to further relax family planning measures to allow three children per couple.

A lesser-known, yet equally formidable challenge is the decline in China’s productivity over recent years.

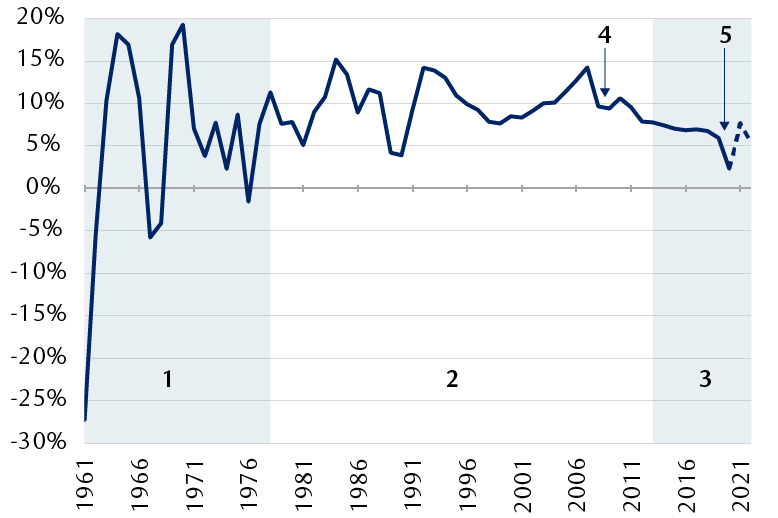

Economic growth is being challenged by an aging population and waning productivity

China’s annual GDP growth, 1961–2020

- 1961–1978: Mao Zedong’s people’s communes have a mixed economic track record

- 1979–2012: Deng Xiaoping’s reforms take hold

- 2013–2022: Xi Jinping prepares China for the next stage of development

- Financial crisis of 2008

- COVID-19 crisis

Source — RBC Wealth Management, World Bank

Reforms and industrialisation spur growth

Starting in the late 1970s, market-oriented reforms produced notable improvements in productivity, enabling large state-owned enterprises (SOEs) to catch up to private-sector productivity levels. This, combined with the move away from agriculture into industry, propelled China’s economic growth to an average of 10 per cent per year until the 2008 financial crisis.

The implementation of these reforms was due in large part to Deng Xiaoping, who emerged as leader within a few years of Mao Zedong’s death in 1976. In a stark departure from Mao’s legacy, Deng dismantled his predecessor’s “people’s communes,” which had destroyed productivity, deciding instead to rely on market forces in the countryside. Many SOEs were closed down, and those that remained were given greater autonomy. Deng allowed non-SOEs to enter the market, and spearheaded the opening of the country to the world, creating competition. Reforms continued into the 1990s, as SOE restructurings deepened and consolidation accelerated.

At the same time, the shifting of China’s labour force from agriculture to industry made higher productivity growth possible. The agricultural labour force, which represented almost 75 per cent of all workers in the late 1970s, declined steadily to less than 25 per cent four decades later.

The expansion of the service economy and the changing role of SOEs

After the 2008 financial crisis, however, the rate of productivity improvement started to fall. A 2020 World Bank report points out that similar productivity decreases also occurred in many other economies due to the waning of the information technology boom, the aging of workforces, and slowing global trade integration. But the report also identifies two factors specific to China: a growing economic emphasis on services, and the role of SOEs in providing “public goods.”

In the wake of the crisis, China started to rebalance its economy away from foreign demand and manufacturing, and towards domestic consumption and services.

The labour force, which had flowed relentlessly from agriculture to industry over the preceding three decades, now began to flow predominantly into services. This weighed on productivity. Services such as finance, leisure, and entertainment are less open to competition and foreign direct investment than industry. With less competition, the productivity of the average worker started to wane across the whole economy. Fewer new firms entered the market, and fewer underperforming companies left the market. The issue was compounded by the growth of non-commercial undertakings such as social and community services, which have inherently low productivity growth.

Moreover, according to the World Bank, SOEs were called upon to fulfill public policy objectives in the aftermath of the global financial crisis, and this also contributed to derailing productivity improvements. It’s important to understand that SOEs play a central role in macroeconomic stabilization in China. Mainly involved in infrastructure construction, they may cooperate with local governments by helping to build and run infrastructure projects — often at the expense of their own financial performance.

Debt-led growth

But this decline in overall productivity went largely unnoticed as economic growth continued at a brisk pace thanks to a large debt-financed public-sector stimulus package. Launched in 2008, it emphasized local government spending on infrastructure and housing as a response to the economic impacts of the global financial crisis. According to the South China Morning Post (owned by Alibaba Group), approximately four trillion yuan ($600 billion) has been invested in infrastructure since 2008.

Local government officials have been strongly incentivized to produce growth in their regions because good economic performance is a major factor in officials’ ability to advance within the echelons of the CCP. This ensures that whoever ends up at the helm of the country has been a successful administrator.

It is this policy of requiring provincial and municipal governments to fund infrastructure projects that has enabled China to keep central government debt at roughly half the level of western nations; according to China’s National Institution for Finance and Development, a government-linked think tank, central government debt totals just 45 per cent of the country’s GDP.

To finance their spending plans, local governments establish companies known as Local Government Financing Vehicles (LGFVs). The governments borrow through these companies, using land assets as collateral. Incurring debt to finance spending is necessary because the power to levy taxes is largely reserved for Beijing. Consequently, securities issued by LGFVs make up as much as 10 per cent of the Chinese bond market.

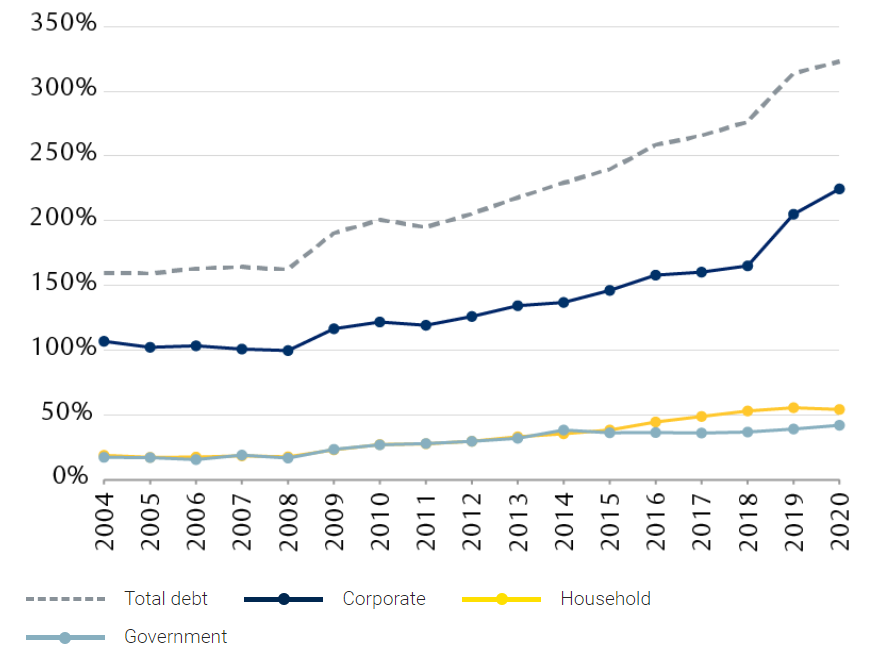

These LGFVs, along with borrowing by SOEs, account for the bulk of Chinese corporate debt—which now stands at an uncomfortably high 200 per cent of GDP. LGFV debts in particular are currently valued at some 40 trillion yuan, or more than $6 trillion, or just over 40 per cent of GDP, according to the International Monetary Fund.

China’s corporate debt level has surged

China debt as a percentage of annual GDP

- Corporate debt includes local government financing vehicles and state-owned enterprises’ debt.

- Household debt is comparable to other countries’ and driven by a growing middle class. Over 50 per cent is mortgage loans. Consumption borrowing has increased rapidly in recent years.

- General government debt is about half that of Western countries.

Source — RBC Wealth Management, Bloomberg; yearly data since 2004

As growth slowed precipitously during the global COVID-19 pandemic, largely as a result of lockdowns imposed to limit the virus’s spread, S&P Global Ratings downgraded the creditworthiness of some LGFVs that had become increasingly reliant on bank loans to pay interest on their bonds. The failure of some SOEs in 2021 further rattled bond markets. The People’s Bank of China kept interest rates at historic lows and ensured liquidity was sufficient to reduce the likelihood of a widespread crisis.

Aware that high levels of indebtedness can imperil stability, China has declared deleveraging and de-risking to be one of its five core government tasks of 2021. It marginally lowered its quota for local government issuance of special bonds, tightened its supervision of LGFVs, and announced that LGFVs should restructure or go bankrupt if they are unable to pay back debt. These measures are likely to encourage LGFVs to deleverage in the medium to long term.

Even so, we see the difficulties surrounding LGFVs as symptomatic of China’s structural challenges. Such a high level of fixed asset investment in infrastructure—as much as 40 per cent of GDP, or roughly twice the world average — will likely prove unsustainable, in our view, given the steady decline in productivity.

Moreover, we see a need for fiscal reforms that better align local governments’ taxation power with their spending requirements. Chinese media have reported that property taxes, already being tried in Shanghai, could be introduced more widely. This would be in line with the stated goals of China’s leadership to redistribute wealth and reduce speculation in hyped sectors such as real estate.

Facing the challenge

China’s growth potential remains higher than that of most developed countries, but we believe its long-term prospects depend on reversing the decline in productivity. The Chinese government seems aware of this, as evidenced by President Xi Jinping’s recent actions.

Much as Deng Xiaoping broke from his predecessor’s legacy, Xi is putting his own mark on the country. While Deng talked about separating the roles of the CCP and the government, Xi has brought them closer together, putting the party firmly in charge of the government and reasserting its control over the economy. As RBC Global Asset Management’s Chief Economist Eric Lascelles points out, this resurgence in the CCP’s authority comes at a time when technology — especially social networks — threatens to usurp some of the government’s traditional influence.

China’s Five-Year Plans

- Annual budgets and economic goals are framed within the context of the current Five-Year Plan.

- Early Five-Year Plans were rigid, setting production quotas for commodities such as steel and grain that had to be achieved by work units.

- Under Deng, objectives became more subtle, indicating the direction in which the Party wanted to steer the country.

- Local governments, state-owned enterprises, and the private corporate sector align their strategies accordingly.

The goals set out in the 14th Five-Year Plan, issued in Nov. 2020, include:

- To reach “high-income country” status, defined by the World Bank as an annual Gross National Income (GNI) per capita of more than $12,700 (it is currently $10,500).

- To pursue President Xi’s “dual circulation strategy” of reducing dependence on foreign markets (especially in the area of technology) while remaining open to the outside world and welcoming foreign investment.

- To achieve stable, equitable and sustainable growth.

- To increase investment in research and development by at least seven per cent per annum.

- To move towards a green economy by reducing dependence on coal and boosting renewables capacity by 40 per cent by 2025; electric vehicles are targeted to make up 20 per cent of new car sales by 2025, from five per cent now.

The stark shift away from the unbridled pro-growth capitalistic approach of the Deng era to one that favours government intervention to promote broader, more stable growth is highlighted in China’s 14th Five-Year Plan, issued in Nov. 2020.

The Chinese government’s recent regulatory crackdown reflects this new direction. Lascelles points out that the new measures appear at first glance to run counter to the goal of unleashing productivity; in the short run, most new regulation will dent company profits and economic growth. But to the extent these rules incrementally reduce corporate concentration, encourage competition, and prune away excesses, they could benefit the economy, society, and financial markets over the long run. He acknowledges, however, that the overall benefits could be tempered by the impact of some measures that seem to be mainly about flexing government muscle.

As Lascelles also notes, similar trends of increased regulation are afoot in other regions. Europe has pursued aggressive antitrust measures against tech giants, and the U.S.—under both President Trump and now President Biden—looks to be tilting in that direction as well. China’s regulatory crackdown could make it easier for the U.S. to pursue its own antitrust measures against the tech sector, insofar as it reduces the risk of U.S. companies losing global market share to Chinese competitors operating under a regulatory regime hitherto seen as more permissive.

Government regulatory crackdown

| Policy goal | Government action | Examples |

| To maintain financial stability | Introduce and enforce anti-monopoly legislation | Internet retailer Alibaba was fined US$2.8 billion in an anti-monopoly probe. Meituan, a food delivery company, was fined US$0.5 billion for violating anti-monopoly regulations. |

| Minimize government intervention and bailouts | Huarong Asset Management, the troubled “big four” state-owned asset manager deemed systemically important, received a $7.7 billion liquidity injection. The government has so far refused to bail out Evergrande, one of the country’s largest property developers, which is struggling to meet interest payments on its $300 billion liabilities, as it sees the risk as containable. | |

| Regulate the FinTech sector | Alibaba-backed FinTech giant Ant Group’s initial public offering was unilaterally suspended, and the group was prompted to restructure as a financial holding company to ensure its financial-related businesses are fully regulated. | |

| Stabilize commodity prices | Authorities announced they would take measures to stabilize commodities prices and crack down on speculation. | |

| Crack down on crypto trading and mining | China’s central bank now considers all crypto-related transactions to be illicit financial activity. | |

| To attain a social democratic form of capitalism, as opposed to the U.S.’s profit-centric capitalism | Protect the vulnerable | Food delivery company Meituan has been required to ensure its workers are paid above minimum wage and receive basic social insurance, and to relax its delivery deadlines. |

| Align business practices with national goals | The lucrative tutoring sector has been barred from earning profits. Prohibitive tutoring fees had become one of the main factors discouraging families from having more children, thereby worsening the country’s demographic issue. | |

| Require businesses to contribute to society | Alibaba pledged roughly US$15.5 billion to support “common prosperity” through programs including improving digital infrastructure in undeveloped regions. Tencent will allocate US$15 billion to social responsibility programs, including medical assistance. | |

| Ensure social impacts are taken into account | China restricted the time children can spend playing online videogames to three hours per week. | |

| To strengthen data security and user privacy protection | Discourage U.S. listing of Chinese companies, to avoid disclosure of information to U.S. regulators. | Ride-hailing app Didi, which had raised funds in the U.S., was removed from the official Chinese app store and told to stop signing up new users until a cybersecurity review has been concluded. |

| Protect user privacy | Concerns that Chinese digital giants were becoming too powerful and mishandling users’ data led authorities to clamp down on powerful tech firms. Ant Group will be required to strengthen protection of users’ data. |

Source — RBC Wealth Management

Other measures, such as redirecting funds from infrastructure spending into productivity-improving investments, should also help China meet its productivity challenge. Xi’s administration has pencilled in $621 billion for research and development spending in 2021, the largest allocation of any country in the world, slightly ahead of the U.S.’s $598 billion. Moreover, China’s acquisition of 783,000 industrial robots in 2019 represented a 21 per cent increase over the previous year; according to the International Federation of Robotics, the country was home to nearly one-third of the world’s installed industrial robots in that year. Such trends, if they persist, could go some way to improving productivity.

Some investment implications

The scale of China’s economy, its contribution to global GDP growth, and its appetite for industrial commodities have made it a powerful locomotive for the world economy and have had transformative effects on most other economies, both large and small. Now, as the country’s leadership seeks to implement a more inward-looking policy mix in order to foster a broader, more balanced domestic economy and regain its competitive edge in the international arena, developments in China are likely to provoke another round of economic effects beyond its borders.

The prospect of a further persistent slowdown in China’s GDP growth into the 3 – 4 per cent range, possibly lower; the shift in policy emphasis away from infrastructure spending toward productivity-enhancing, technology-driven investment; the drive to promote renewable energy development as a way to reduce dependence on foreign energy imports; and the crackdown on unconstrained capitalism and conspicuous wealth in favour of broader gains for the average citizen—we believe all will have important ramifications for those trying to do business in China, as well as for those competing with Chinese firms in the global marketplace.

A more difficult market to penetrate. After Deng exhorted the Chinese people to strive to “get rich,” a cachet quickly developed around the possession of well-known global brands — from burgers to jeans, to designer clothing, to pricey Bordeaux wines and luxury cars. But in recent years, domestic brands have emerged and, backed by digital marketing, have rapidly gained a commanding market share. In the luxury goods space, where global brands have feasted for thirty years on the wealth of a rapidly expanding Chinese middle class, conspicuous consumption is no longer lauded as evidence of China’s arrival as a global economic powerhouse. Unbridled wealth that is not aligned with the direction and goals set by the country’s leadership is likely to be discouraged. “Access to the China market,” coveted by many global businesses and always difficult to achieve, looks to become even more difficult in light of the goals set by China’s leaders.

Diminished outlook for industrial commodities. A reduced emphasis on infrastructure spending as a way to achieve regional growth targets, along with what appears to be a forced deleveraging of the very large property development sector (where a large proportion of the need for modern housing has already been met) could mean a slower uptake of many industrial commodities. An important brick in the wall of the “commodity supercycle” thesis has been the expectation that infrastructure development would remain the preferred mode of fiscal stimulus in China. In the event, infrastructure does not feature among the major goals of the current Five-Year Plan, there are indications it will be used more sparingly and deliberately going forward.

Productivity-enhancing investment by China will require a competitive response by developed economies. The wholesale relocation of production facilities to China by global manufacturers ended some years ago, as global firms faced numerous difficulties including arbitrary, rapidly changing regulations; logistical challenges; poor technology security; and the rapid escalation of Chinese labour costs. If China’s heavy investment in productivity-enhancing capital goods proceeds at the pace encouraged by its leadership, manufacturers and other businesses around the world will have to respond in kind.

In our view, key trends driving global change today will continue into the future: the digitization of everything that can be digitized will accelerate, robots will become more ubiquitous and extend their reach into small and medium-sized businesses, and artificial intelligence will be embraced as an essential competitive tool. It is unclear whether all this will yield the necessary productivity gains — for China, or the rest of the global economy—but if the “other guy” is spending big on what looks to be a transformative technology or product, then it may simply be too risky for competitors not to keep pace. Another long stretch of heavy, tech-driven spending likely lies ahead.

This article was originally published on rbcwm.com

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.